Maple Finance - Research Report (from November 28, 2021)

The next critical driver for institutional decentralized finance adoption - in 5 years' time it will just be called 'finance'

Disclaimer: I am invested in MPL. This is not investment advice. This report includes illustrative estimates and is for informational purposes only. You should not make decisions based solely on this report nor misconstrue this as a recommendation to purchase MPL. Further, this report was written in November 2021 prior to any discussions related to joining the Maple team.

If interested in discussing anything further, please reach out to me via Twitter @qthomp. This report was originally furnished in a nicer looking pdf file so happy to provide that as well.

TLDR:

Maple Finance (MPL) is an institutional capital markets platform providing undercollateralized lending for institutional borrowers and fixed income investment opportunities for lenders.

The long-term vision of the protocol is basically a combination of JPMorgan’s debt capital markets desk plus Blackrock’s array of fixed income investment products in a one-stop shop built on the blockchain. Today, the platform originates and syndicates loans debt to high-quality institutional borrowers while also providing individuals and institutions access to invest in these fixed income opportunities via diversified or single-name pools.

Maple allows for more efficient access to capital for institutions while at the same time increasing transparency and accessibility for investors.

The protocol is governed by the Maple Token (MPL) which enables token holders to participate in governance, share in fee revenues and stake MPL to the various lending pools, effectively acting as insurance / first loss capital and in turn receiving outsized compensation for it. The platform currently operates a number of USDC lending pools that are semi-permissioned. Lending and staking is fully permissionless – i.e. anyone with a Metamask wallet can provide liquidity or be a Staker (aside from the two specific fully-permissioned pools). Borrowing is fully permissioned however with Pool Delegates acting as fund managers – onboarding potential borrowers, financial analysis and due diligence, credit underwriting and negotiation and ongoing risk monitoring.

Maple is a protocol building a serious moat and brand reputation.

It is not a project that can simply be forked given the relationship driven nature of the business and the human capital required to successfully operate. In about six months of operating, it has gone from zero to over $400mm of sticky TVL that has a minimum 90 day lockup. Unlike other overcollateralized lending and borrowing protocols in DeFi today, Maple’s TVL isn’t artificial either. The supply and demand aspects are real and are not simply derived from token reward farming or rehypothecated assets in the protocol. The team has grown to over 20 people including backgrounds from Maker, Microsoft and Accenture (development), TikTok (marketing) and capital markets/structured finance.

Maple’s early success and continued rapidly expanding TVL will come from:

A total addressable market measured in the trillions with an insatiable demand from institutions to borrow

Increased market education and adoption of high-quality undercollateralized lending as a reliable and safe source of yield for both institutional and retail investors

Top tier team with strong backing across the industry, with a clear focus towards building a scalable platform

Profitable business with sound tokenomics that offers a sustainable source of yield for lenders

Near-term opportunities to expand business lines and new product features to capture additional market share

Protocol Overview:

Who uses Maple Finance?

Institutional borrowers – today consists of crypto native businesses including market makers, OTC desks, banks and investment funds but will expand to miners, DAOs and non-crypto natives

Lenders – anyone with a Metamask wallet (individuals or institutions) seeking to access a diversified yield derived from high-quality borrowers

Pool delegates – credible asset managers who launch and manage lending pools; conducting due diligence, underwriting borrower credit risk and negotiating terms with creditworthy borrowers

Stakers – anyone with an Ethereum Metamask wallet (individuals or institutions) who stake tokens into pool staking locker contracts to provide first loss capital in the event of default and in return receive a percentage of interest earned by the lending pool

Protocol Mechanics

Lending

Lenders (anyone institution or individual with a Metamask wallet) deposit USDC into one of the pools based on their preferences for counterparty type and risk/reward

In return, lenders receive a corresponding Maple Pool Token (MPT) representing their share of the pool. These MPTs are then deposited into the Liquidity Mining contract to earn their share of USDC interest and MPL rewards

As interest is earned, it is reinvested by the pool – compounding interest

Earned interest can be claimed at any time however principal withdrawal must meet minimum lock period of 90 days + 10 day cooldown which allows for effective liquidity and utilization management

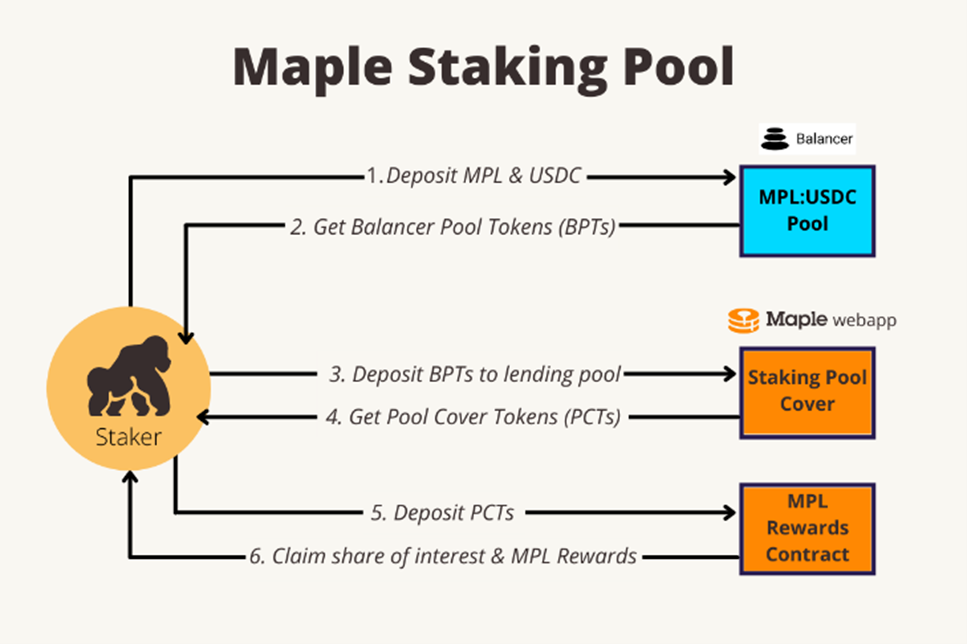

Staking

Stakers add value to the staking locker contracts which serves as a first loss reserve that can be liquidated to protect lenders in an event of default and thus reduce their risk of loss given default

As compensation, Stakers earn a percentage of the interest paid by borrowers to the pool that would have otherwise gone to Lenders

To participate, Stakers deposit both MPL and USDC to the MPL:USDC 50:50 Balancer Pool in exchange for Balancer Pool Tokens (BPTs)

Users do have option to deposit only one asset, however you get a worse value than if depositing both assets which stems from the price slippage required in the backend swap to the multi-asset format

The BPTs are then staked to the user’s choice amongst the corresponding lending pools – in return users will receive Pool Cover Tokens (PCTs) which represent their share of the first loss reserve and will begin to accrue USDC yield, plus MPL rewards once the PCTs are deposit into the MPL rewards contract

Staking currently receives 10% of the interest yield in a pool plus MPL rewards

APY from MPL rewards will vary depending on the volume of MPL staked and the MPL price with a monthly calculation to target a staking reserve size of 8-12% of the balance of pool liquidity

MPL rewards are sized to hit a target all-in APY consistent with current market conditions (~15-20% today)

Target all-in APY is calculated as USDC fee + MPL rewards. Current market conditions for stablecoin farming are ~15-20%.

As an example: If a pool’s average interest rate is 10%, 1% goes to Stakers and if the staking reserve is 10% of loans outstanding, then the USDC APY to Stakers is 10% (i.e. 1% / 10%), so to achieve a target all-in APY of 15-20%, target MPL rewards would be 5-10%

MPL rewards implementation will be a fixed number of MPL to the staking rewards contract at the start of each month based on 1) avg MPL price over preceding 7 days, target staking volume in protocol for next month, target all-in APY that month and average interest rate on loans in the pool

(Update as of January 2022: This workflow will be simplified and optimized once single sided staking is rolled out as discussed on recent team communications in Discord, Telegram and community call)

Pool Delegates

Seek approval by Maple governance to launch a pool contract, attract capital and commit loans

As compensation for their work in managing the pools, Pool Delegates receive pool-specific portion of the interest accrued from borrowers and 50% of establishment fees taken upon drawdown of each loan associated with their pool

Borrowing

Interface allows for borrowers to create borrowing request, onboard and provide company information/requested diligence items, facilitate discussions and negotiations with pool delegates, execute loan documentation, post required collateral, disburse loan and pay interest and loan principal

Protocol Parameters

Static: Liquidity asset (asset used for a pool to lend to borrowers and accept as interest), delegate fee (% of interest generated by pool that is allocated to delegate), staker fee (% of interest generated by the pool that is paid to stakers)

Flexible: Pool capacity (maximum pool size), liquidity and staker access (public or privately whitelisted only availability), lockup period (minimum time liquidity must be locked prior to withdrawal – currently can be decreased but not increased)

Global (first specified by Maple core team and eventually will be determined by broader Maple governance): Establishment fee (% paid by borrowers for each new loan origination and split between treasury and delegate recipient), cooldown period (time required to pass after LP or staker initiates withdraw)

Revenues & Tokenomics:

There are two main sources of revenues, Establishment and Ongoing Fees, that are split across the three key stakeholders – Lenders, Stakers and Pool Delegates.

Establishment Fees

Establishment Fees (also known in TradFi as origination, upfront or arranger fees) are paid by Borrowers at the initiation of each new loan; today this is 0.5% of the principal amount of the loan

The Establishment Fee is split 50/50 between the Maple treasury and the respective Pool Delegate

Ongoing Fees

Ongoing Fees are the interest paid by borrowers on the loan principal amount

80% of the Ongoing Fees are paid to Lenders, 10% to the respective Pool Delegate and 10% to Stakers

For MPL holders to earn the additional fees via participation in the Ongoing Fee, MPL tokens must be staked to a Lending Pool, thus acting as first loss capital

Summary of Revenues

Lenders: 80% of Ongoing Fees

Pool Delegates: 50% of Establishment Fees and 10% of Ongoing Fees

MPL Stakers: 10% of Ongoing Fees

Maple treasury: 50% of Establishment Fees

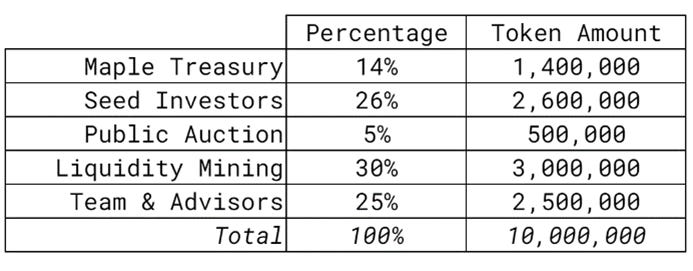

Total and Circulating MPL Supply

10,000,000 fixed MPL token supply minted on April 20, 2021

2,878,157 MPL tokens in circulation today (~29%)

Estimated 3.3M liquid MPL tokens (~33%), which may not all be in circulation yet

~1,300,000 from seed investors (13%)

Seed round conducted in October 2020, raising $1.3M, for ~2.6M MPL at $0.5 per MPL

5% unlock at Token Genesis Event (TGE) and 18 month linear vest (~50% unlocked as of 12/1/2021)

500,000 from public auction (5%)

~380,000 from treasury (3.8%)

Jan 2021: Strategic OTC raise from Treasury for $1.4M at $3 per MPL with 12 month linear vest from TGE (~67% unlocked)

Mar 2021: Strategic OTC raise from Treasury for $0.5M at $5 per MPL with 12 month linear vest from TGE (~67% unlocked)

Estimated ~650,000 from liquidity mining (6.5%)

Estimated ~500,000 from team & advisors (5%)

Investment Highlights and Catalysts:

A total addressable market measured in the trillions with an endless demand from institutions to borrow.

As of October 2020 there is ~$22 trillion outstanding debt across the globe that is rated by S&P Global Ratings with ~$2 trillion per year issued in the U.S. corporate market alone. Obviously it will take some time for all of that to come on chain, but nonetheless DeFi lending is already in the billions today and I would estimate the institutional crypto lending market is ~$50+ billion. As of Q3 2021, Genesis by itself has $11 billion of outstanding loans and originated $36 billion of new loans in Q3 alone. Today, Maple Finance’s borrower network is completely global, spanning 10+ countries in North and Latin America, Asia, Africa, and Australia. Across other CeFi crypto lenders like BlockFi, Celsius, etc. is probably another ~$25-50 billion in AUM today.

Increased market education and adoption of high-quality undercollateralized lending as a reliable and safe source of yield for both institutional and retail investors.

Institutional lending and corporate debt markets are not widely understood concepts for average individuals. Today in crypto the types of leverage that exist are overcollateralized DeFi borrowing with variable rates, overcollateralized CeFi borrowing with fixed rates and exchange margin/leveraged trading/futures. An easy talking point for many people is around all of the ‘leverage in the system’ as displayed by futures open interest and funding rates. The fact that this leverage exists and is a large part of crypto markets today is true. But what people don’t understand is that this is a fundamentally different type of debt/leverage than institutional fixed term borrowing, of which makes up most of the trillions of dollars in outstanding debt in TradFi. Given this lack of understanding, people don’t understand the risks and therefore have difficulty conceptualizing what the expected return should be (evidenced by the discussion from the recent Merit Circle proposal to invest treasury funds into a Maple lending pool). Building awareness in the crypto community about the importance of institutional capital markets and demystifying this term ‘leverage’ will go a long way towards adoption. The crypto native borrowers today typically operate in a secret manner and disclose as little information as possible so transparency needs to grow over time as well (service providers such as X-margin should help with this).

Top tier team with strong backing across the industry, with a clear focus towards building a scalable platform.

Institutional lending is still very much a relationship driven business and although Maple Finance was not first to market, they have established themselves as the leader in the nascent uncollateralized DeFi subsector due to their strong reputation and leadership team. The team is over 20 today, comprised of professionals with years of capital markets / structured finance experience and backgrounds such as Microsoft, Accenture, Maker and Tik Tok on the development and marketing side. Demand for undercollateralized from institutional borrowers is well-known, but to become a large, scaled platform there must be a heavy emphasis on high quality counterparties, risk management and appropriate underwriting to properly align incentives and protect lenders. Unlike TrueFi and Clearpool, Maple is outsourcing the credit review and underwriting process to well-known Pool Delegates who have years of lending and industry expertise which allows Maple to act as a facilitating platform versus actually allocating capital and directing credit decisions. This segregation of duties may not seem important today however it allows for a more scalable and sustainable business model. It not only leverages the capabilities and networks of its reputable Pool Delegates but also reduces the risks of spillover effects from a potential default. Exogenous events and defaults are inevitable and it’s important that these outcomes are not tied to Maple’s processes and do not affect the viability of the platform as a whole.

Profitable business with sound tokenomics that offers a sustainable source of yield for lenders.

Debt capital markets and institutional lending is no novel invention, however the current TradFi model is ripe for disruption given the number of rent seekers throughout the process from arrangers, underwriters, syndicate banks, admin agents, trustees, asset managers and investment vehicles. Additionally, there is a funding shortage across crypto native firms and protocols as they do not have the availability and access to large pools of capital. There is clear product market fit from both a yield generation and borrowing perspective and Maple has built a protocol model that aligns incentives among Lenders, Pool Delegates and Stakers. The nuances around economic fee splits amongst the different stakeholders is extremely important given the principal / agency dilemma. Pool Delegates must have skin in the game and responsibility for credit decisions and earn the trust of Lenders and Stakers who are providing capital. Institutional lending is also a very sustainable source of yield, especially when compared to most of the other DeFi yield opportunities that are largely driven by inflationary token rewards. In addition to the economic value capture the MPL token receives, its design provides for organic demand to hold the asset as it is required by Stakers to receive additional yield.

Near-term opportunities to expand business lines and new product features to capture additional market share.

Maple already has over $400mm TVL lent across a network of 30+ borrowers in six months since launch. The amount of large scale crypto native businesses is growing rapidly and presents an untapped area of the market with probably another 30 borrowers that can be onboarded over the coming six months. The team has an ambitious product roadmap, with several the near-term initiatives outlined below that will serve as catalysts for the platform:

Single-sided staking option

Today Stakers seeking to earn a yield (paid in USDC+MPL) by providing Pool Cover can only stake with a 50:50 split of USDC and MPL. There are reasons it was originally done this way but the team is also working to add single sided staking in the form of ETH, WBTC or MPL. This will provide users the ability to earn a yield on their other assets that are returning much lower yields elsewhere and also bolster the stability of the lending pools for lenders by providing additional first loss capital. It also helps mitigate MPL token price risk in a liquidation event because it diversifies the asset pool and will reduce purely MPL selling pressure.

Additional Pool Delegates and specific lending pool types

Current borrowers largely consist of crypto native businesses like market makers, OTC desks, crypto banks and investment funds however increased capacity can be brought onboard by expanding to miners, DAOs and non-crypto natives. The DAO opportunity set is one I am particularly keen on as it is a rapidly growing part of the market with a growing need for capital markets access via DeFi.

Single-name pools in addition to the inaugural Alameda pool

This can be compared to syndicated loans or bonds from the TradFi world and effectively begins to build out the credit risk premia for borrowers across the crypto ecosystem

Other tenors, both shorter and longer than the current 90 day term

As more borrowers onboard to the platform, capital needs and asset/liability duration matching will vary. This will serve to build out the yield curve within the crypto ecosystem. Most institutional lending in crypto is done on an open term basis (i.e. ~3-5 day put/call periods).

Other asset pools, beginning with BTC and ETH with the potential to add to list of assets as demand supports it

Within crypto today there is massive institutional demand to borrow BTC and ETH in addition to stablecoins. This market today is likely upwards of $10+ billion and will continue to grow with adoption. Adding lending pools specific to assets aside from USDC will offer a yield for users’ other assets and provide additional capital to the borrowers already onboarded to the platform borrowing billions of these assets via CeFi.

Additional financial products and instruments

Insurance, derivatives, CDS, indices and other fixed income investment products

Integration with service providers like X-margin to incorporate real-time and transparent borrower reporting and risk monitoring

Competitive Landscape:

Among its DeFi competitors, Maple’s early success comes down to its product market fit and UI/UX. Given institutional lending is already a relatively unknown area to the average individual, Maple’s straightforward approach has resonated with lenders and borrowers. Aspects like TrueFi’s bonding curve to exit liquidity pools and Clearpool’s dynamic interest model introduce potentially unnecessary complexities that may add to fragility in times of market stress. The CeFi landscape benefits from user’s familiarity with centralized institutions, easiest on/off ramps from fiat and ease of use.

CeFi

Maple’s largest competitors today come from the CeFi crypto lending space (i.e. Blockfi, Celsius, etc.) who combined have ~$25-50 billion in AUM

CeFi “crypto banks” or exchanges serve as most individuals first foray into crypto and therefore benefit from large user bases and sticky deposits

As the institutional presence in crypto increases, the demand for decentralized protocols and diversification of counterparties will help DeFi continue to gain assets

Overcollateralized DeFi (Aave and Compound)

Only overcollateralized lending with variable interest rates based on utilization rates largely catering to individuals

Launch of Aave Arc and Compound Treasury to cater to institutions however more so focused on the depositing side

TrueFi

The biggest difference is TrueFi operates under a credit scoring model with a credit review done by the TrueFi team and borrowing decisions effected by a community votes;

Lower utilization rates around ~55% with excess is deposited into Curve.fi y pool to earn yield

Staking receives 100% of protocol fees which consist of 10% of all interest generated (bullet payments) with a loss capped at the staked TRU Maximum Liquidation Rate

Where Maple excels is despite TrueFi maybe taking a more ‘decentralized’ angle with the community voting mechanism versus the Pool Delegate model, institutional lending requires expertise and proper information. Because the community is not receiving borrowers’ financials and access to due diligence findings, they are not properly equipped to accurately assess and vote upon credit decisions. This makes it overly favorable for borrowers and sets individuals and lenders at an informational asymmetry disadvantage. The path to fully decentralized lending needs to be a gradual one.

Clearpool

Single name borrower liquidity pools with dynamic interest rate model that function based on the pool utilization rate

Will have ‘thematic pools’ that offer diversified risk exposure in the future

Revenues and tokenomics unclear

Where Maple excels is that Clearpool’s underwriting process and interest rate model that is a function of pool utilization introduces variability for both lenders and borrowers that is not actually tied to the underlying credit risk being taken. For lenders who seek fixed interest rates for clarity there is the risk that due to an idiosyncratic pool liquidity issue their cost of capital could be significantly affected. And vice versa for lenders the actual yield earned will deviate from the risk being undertaken. Clearpool’s integration with X-margin is an interesting development that could lead to increased transparency and a better protocol.

Goldfinch

Focused on providing leverage against off-chain, real world assets

Auditor protocol model yet to be proven out

Valuation:

The above metrics consider fully diluted values across the DeFi protocols. A few important value drivers to point out:

Maple’s P/S and P/E metrics are quite lower than the other DeFi protocols

The undercollateralized lenders, Maple and TrueFi, have much higher P/TVL metrics when compared to their overcollateralized lending counterparts, Aave and Compound. This makes sense given the profitability and efficiency of TVL usage; additionally, a portion of Aave and Compound TVL can likely be chalked up as rehypothecation

Maple’s value capture and tokenomics are some of the most profitable and efficient out of both the overcollateralized and undercollateralized DeFi competitors

Maple also boasts a TVL utilization rate of nearly 90% whereas TrueFi’s is closer to 55%

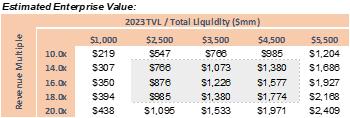

Looking out to 2023, it’s likely that TVL continues to rapidly scale. As crypto adoption grows broadly and DeFi along with it, capital will continue to flow into the space from the tens of trillions of dollars sitting in the TradFi world earning near zero rates of return. Additionally, it’s likely that the market capitalization of the crypto majors like BTC and ETH eclipse $4+ trillion (from $1.5 trillion today). For context, $1 billion out of $4 billion is 2.5 bps, or 0.025%! Granted the economic benefit of these assets for the protocol is not as impactful given their lower interest rates, the near-term addressable market is likely much larger given they are crypto native assets already moving across the blockchain.

Recent MPL price action:

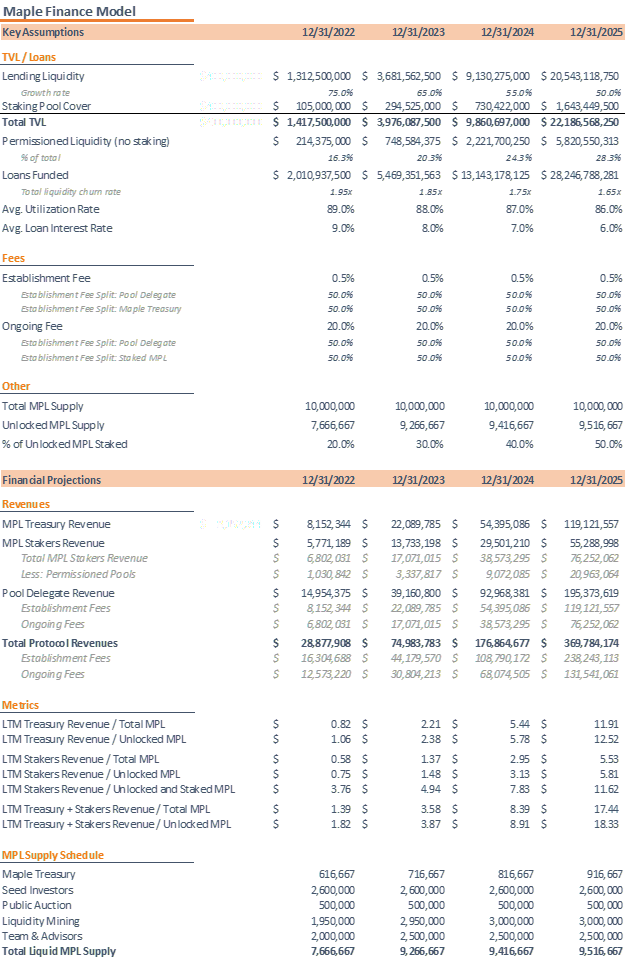

Illustrative projection model:

Key Risks:

Smart contract risk

As with any DeFi protocol there is a risk of smart contract bugs and exploits. Maple has a number of features that mitigate this risk.

Audits conducted by Peckshield, Code Arena and Dedaub (Trail of Bits audit is due Wednesday 12/1)

High pool utilization rates (~90%) make Maple’s smart contracts unattractive targets given the small reward

90 day lock up plus 10 day cooldown period for lenders (reduces risk of flash loans and other exploit attacks)

Credit risk

The risk of default or lending to borrowers who are not creditworthy is probably the largest risk to the protocol, particularly in the near term as it is getting off the ground. It is important to have Pool Delegates who are knowledgeable and credible risk managers as they are performing the underwriting process to assess new borrowers, monitor markets and negotiation of loan terms. It is also important that Pool Delegates incentives are properly aligned with Lenders and Stakers given there is a principal / agent dilemma. Pool delegates are also responsible for other portfolio management aspects such as liquidity (matching balances in pools for the appropriate asset / liability durations) and special liquidations in event of default.

Pool Delegates are paid via establishment fees (one time at origination of loans) and a portion of ongoing interest earned from their pool. as they are required to stake MPL to their lending pool to serve as a reserve of first-loss capital. In order to properly align incentives, Pool Delegates are required to stake a minimum of $100k in value to their Pool Cover acting as first loss capital. This will become particularly important to monitor going forward as the pools grow in size – particularly maintaining an appropriate Pool Delegate revenue in relation to required risk capital.

The default risk is mitigated via the Pool Delegates’ borrower selection. The firms who borrow today are extremely profitable with very strong balance sheets. They primarily derive revenues from market neutral strategies that are not dependent on crypto price appreciation. The firms are large, well-established players in the space and given the transparent nature of the outstanding loans are seriously incentivized to not do anything that would inflict on their reputation. Other risk management techniques such as concentration limits are in place to reduce risk.

In the event of a default, the first loss capital in the pool cover which is typically 8-10% of total pool liquidity is a meaningful protection for lenders. Obviously in this case the Stakers get hit but that is the risk going in and hence a higher return potential.

Source of yield

The sustainability of the high APYs is important when evaluating DeFi protocols. For Maple, there is strong demand around ~10% APY today for institutional borrowing. This is highly differentiated from current overcollateralized DeFi protocols where I would say a lot of the demand is ‘manufactured’. Additionally, there is a demand for institutional borrowing no matter the conditions of the crypto market. Borrowing and lending is a core piece to efficient capital markets and businesses’ balance sheets, particularly for market makers, OTC desks and trading companies who are dependent on the leverage and 0% collateral model. Market Makers will not use overcollateralized loans because their business relies on very high utilization of capital combined with the leverage and market neutral approach which makes it highly inconvenient to post any collateral.

MPL price risk in event of default / liquidation

In the event of default, the Pool Delegate will liquidate the MPL in the Pool Cover (either via AMM or OTC) as needed to offset any losses from default. The speed and execution of this is critical and remains to be done in practice, creating a potential risk factor for the protocol if not handled properly. The other consideration is the liquidity of the MPL token and the size of the Balancer pool (which today stands at ~$17mm - $8.5mm USDC, $8.5mm MPL). In a meaningful event of default today, this would be a large MPL sell event into stablecoins and would cause serious downward pressure on the MPL token price (not to mention the other potential negative effects a default would have on the protocol’s users). This risk will be mitigated by additional listings on centralized exchanges that will improve liquidity and new tokenomics features that allow for multi-asset staking.

Leadership team and protocol governance

The Maple leadership team is highly visible, communicative, and transparent. They are visible and include the community in relevant discussions via Discord, AMAs and weekly updates. The risk of poor management or bad actors is very low here.

Links and Resources:

Podcasts / Appearances

1/13/2022 Ep 46 | Decentralized Credit & Capital Markets with Sidney Powell of Maple Finance

8/21/2021 Institutional Lending in DeFi Panel

Maple in the Press

1/27/2021 Bankless DeFi Innovation Index $GMI

1/20/2022 Maple Finance acquires Avari (link, link)

1/10/2022 Mave 11 Pool Reaches $175 million

11/25/2021 How Zombie Companies and Cheap Credit are Stifling Innovation | The Fintech Times

11/21/2021 Merit Circle Proposal

11/18/2021 First Defi Syndicated Loan

11/8/2021 Pickle Finance uses Maple as its treasury solution - DeFi Report

11/7/2021 KIP-6: Yield generation on Maple Finance

10/21/2021 What It Takes to Run a Crypto Hedge Fund | Real Vision

Latest Blog Posts / Roadmap

1/20/2022 Maple Finance acquires Avari for rapid launch on Solana

1/7/2022 To come in Q1: A more usable, interoperable and valuable Maple Finance

12/29/2021 2021 in review: building, launching and growing Maple Finance

Research on Maple

9/15/2021 How Institutional DeFi is evolving - what & who you need to know

6/21/2021 Maple Finance: Bringing Undercollateralized Lending to DeFi | Messari

1/20/2021 DeFi will eat corporate debt - Bankless

Latest Weekly Update

1/21/2022 ICYMI

12/14/2021 Sunday Syrup

Community Call

1/29/2022; 12/15/2021 slides and video

Financials

Audits

Github, Peckshield, Code4Arena, Dedaub, Trail of Bits coming soon