The Case for ETH

Ethereum has suffered from being the 'middle child' to Bitcoin and Solana, culminating in a capitulation event on the eve of the Bitcoin ETF approval, however the prospects look much better now.

A few weeks ago I tweeted a brief summary of the ETH/BTC bull case but wanted to elaborate further.

Introduction

First let’s set the stage. Bitcoin and ETH are ~30% and ~55% gains away from ATHs, respectively. On a relative basis, the ETHBTC cross is at ~0.06 with the previous cycle high being ~0.085 seen in December 2021.

This cadence is pretty typical early in bull markets. Bitcoin leads the way, followed by Ethereum and then the rest of the alt complex. See the white vertical lines above in February 2017 and December 2020 - in both cases Ethereum outperformed Bitcoin by over 2x in the ensuing 6 months. I believe we see another period of relative ETH strength once again.

But surely we must be missing something? How could the market be affording this setup despite two historical analogous situations? For the last two years I have believed ETH to be over-owned as it was everyone’s go-to “set and forget” allocation. It suffered because it became too consensus. That has now changed and the reasoning lies behind the one-two punch delivered by the Great Solana Repricing of 2023 and the Bitcoin ETF Hysteria. Let’s dive into each.

The Great Solana Repricing of 2023

Beginning in the summer and accelerating more forcefully post-September, SOL went on a tear. Despite being left for dead by SBF and staring down a large supply headwind from the FTX estate, the Solana community awoke from the bear market stronger than it went in. Development activity persisted, user counts and transaction activity continued scaling and new protocol began sprouting left and right.

This resurgence caught the market off guard and set the stage for SOL’s almost 5x outperformance over ETH in 2H 2023. Naturally Solana’s success revived the “ETH killer” narrative as many predicted its demise to the newer and faster smart contract blockchain network. Many in this camp point to its unfriendly user experience stemming from higher transaction costs and slower confirmation times. After locally peaking at ~20% of ETH’s market cap in late December, Solana has retraced back down to 12%. This was the first punch that put ETH’s performance under pressure.

Although ETH may operate a bit ‘clunkier’ than Solana, its important to recognize the flurry of activity and building occurring within its ecosystem with Layer 2’s leading the way. “You come at the king, you best not miss”.

Bitcoin ETF Hysteria

The knock-out blow causing final capitulation in the ETH/BTC ratio was delivered with the approval of the Bitcoin ETF. Unsurprisingly as the Bitcoin ETF approval became more likely, market sentiment and positioning favored it heavily. From the day Blackrock submitted their application to the eve of approval, ETH underperformed BTC by ~33%.

Numerous times during the run up to the approval, ETH saw moments of strength as the green shoots of the “ETH is next” narrative emerged. Funny enough, these brief periods of strength typically signaled local tops coinciding with market exuberance.

All the while Solana was rapidly scaling market share and out of this combination the “ETH is a cucked coin” narrative was born. It was losing to both Solana and Bitcoin in risk-on and risk-off environments, respectively, leaving many unable to justify its spot in a portfolio.

As a follow-on, the strong showing of inflows into the Bitcoin ETFs is keeping many on this path of ETH skepticism, not wanting to fade the asset with a newfound conduit for inflows that ETH does not yet have.

The ETH ETF

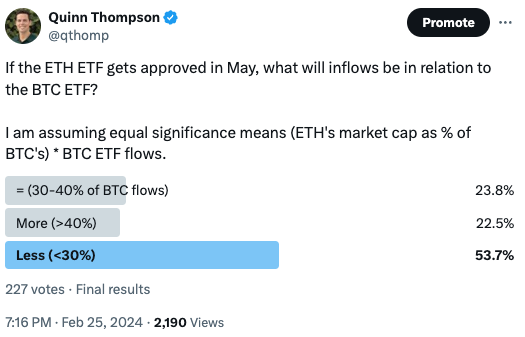

With the Bitcoin ETF launches behind us, the market has slowly turned its attention to the late May ETH ETF deadlines. The consensus is rather uncertain whether or not it will get approved. A poll I ran on Twitter showed as much with a slight skew 50.7 / 49.3 skew to a sub-50% likelihood of approval. Basically the market has no idea.

On top of that, it is also unclear what consensus is on expected flows upon approval. I often hear both sides of the argument with some citing the lack of demand for EFUT (only $22M AUM) and others pointing to ETH’s institutional characteristics resulting from DeFi and tokenization.

The situation is highly uncertain with many well-respected market participants and lawyers taking different sides.

ETH Will Outperform BTC Regardless

Let me explain why the ETH ETF decision is a distraction and will lead many to overthink this trade.

Consensus does not expect the ETF to get approved in May

Consensus expects the flows to be less significant than BTC’s *if* it were to be approved in May

There seems to be a resounding consensus on its approval by this time in 2025 if it does not happen this year (largely due to a similar litigation route that Grayscale went down for the BTC ETF)

So right out of the gates your downside is limited if the ETH ETF is denied or delayed because the market expects it to either not happen or garner less significant inflows if it did. Obviously this would affect ETH’s price, but if it were to occur today I think it would be a buying opportunity.

Now let’s get into the more important drivers.

Stablecoin supply growth: I’ll leave you to arrive at any conclusions from the below charts but there’s obvious linkages. The vast majority of stablecoins live on the Ethereum blockchain and their supply is an coincident indicator for user count and transaction activity. YTD 2024 stablecoin supply has grown over +1% per week on average. From a $126B starting point across USDC and USDT, this is >$1B per week and a pace of >$60B for the year. For avoidance of doubt, there are no stablecoins on the Bitcoin blockchain.

USDT supply (dark pink, bottom), 60D rate of change (light pink, top), ETH/BTC (green, top)

USDC supply (dark pink, bottom), 60D rate of change (light pink, top), ETH/BTC (green, top)

Inflecting On-Chain Activity: The sole reason for ETH’s outperformance during bull markets is its relative ‘operating leverage’ to on-chain activity. Growth in crypto adoption benefits Ethereum in an outsized way due to its role as the leading smart contract blockchain network. Higher adoption leads to exploration into the technological use cases beyond Bitcoin, resulting in growing transaction volumes and activity on Ethereum. Trading volumes serve as a good barometer for broader activity levels. They began to pick up in Q4 2023 but are still less than half of the peak levels seen in 2021. Any uptick from here will benefit Ethereum as its the category leader in almost all key use cases - DeFi, NFTs, etc.

Additionally, higher throughput leads to more fees and more ETH gets burned as a result. Aside from the September and October doldrums last year, ETH’s supply has been deflating and currently sits at July 2022 levels. For context, Bitcoin’s supply has grown +2.8% in that time frame. Since the merge in September 2022, ETH has averaged -0.212% of annual supply deflation. On a 7-day and 30-day basis the annualized rate stands at -0.447% and -0.262%, respectively. I reckon it’s fair to say deflation will pickup in a bull market.

Dencun Upgrade: Scheduled for March 13th, EIP-4844 improves throughput while reducing transaction costs for layer 2’s, helping to streamline the ecosystem’s move to rollups. While the standard for past ETH upgrades and other large events in crypto is “buy the rumor, sell the news”, it is difficult to argue there has been any “buying of the rumor” in this instance. Meanwhile the upgrade directly addresses Ethereum’s scaling solutions making it more competitive against Solana’s strengths.

Additional Demand Drivers and Coinciding Supply Sinks: While over 25% of ETH’s supply is now staked, there are a number of other catalysts taking place with re-staking and Layer 2’s. The percentage of ETH staked, re-staked, locked in smart contracts and bridged to Layer 2’s is at an ATH. Example’s include Blast’s $1B in deposits before going live ($2B+ currently) and EigenLayer’s $8B+ at the time of writing this. Events like these increase the demand to own Ethereum and act as near-term ‘supply sinks’.

The Charts Say So: If none of that gets you excited, let’s look at how things are playing out relative to previous cycles.

Bitcoin dominance (which is largely an inverse ETH/BTC line) appears to be rolling over.

ETH/BTC has bounced off its large trend line and moved above the 200WMA.

On a length of time basis, the correction in ETH/BTC has been significant, although on a relative value perspective it has not been as deep. Regulatory Momentum: Aside from many getting lost in the weeds on whether or not an ETH ETF is going to happen this year, I see the bigger picture to be the overall progress being made on the regulatory front which undoubtedly benefits Ethereum. Last fall we got the first ETH futures ETFs and we’ve seen a number of large-scale SEC losses in the courts that is a turn in sentiment from the past few years. The January Coinbase hearing was another step in the right direction and the upcoming ruling could be another positive catalyst. Last week’s Uniswap fee switch proposal is potentially another signal of thawing regulatory fears. In summary, the momentum is positive and progress is being made towards clarity which is a major benefit to the ecosystem.

The Trade

Over the long-term, your guess is as good as mine, but I feel pretty comfortable saying ETH will outperform BTC over a 6, 12 and 24 month time horizon. For context, the last two times Bitcoin’s dominance was at current levels (52-53%), ETH’s dominance has continued to grow.

While the conceivable traditional analogy for Bitcoin in the near-term is a digital version of gold, Ethereum’s is much greater. While difficult to quantify the value of the internet, it is certainly larger than the market cap of gold. The long-term vision of Bitcoin becoming a reserve currency or medium of exchange more akin to the dollar is likely further away than all of the top technology applications being built on top of smart contract blockchains like Ethereum. As of today I expect the value of Ethereum and/or another winning smart contract blockchain to outpace the growth of Bitcoin largely due to this factor.

0.07 is the next logical target as much of 2021 and 2022 were spent trading around that level. I think this level is hit by the end of April regardless of an ETH ETF approval. I am envisioning a $4.1k ETH / ~$59k BTC coinciding with that level.

My thoughts on how the ETH ETF decision play out are as follows:

The SEC is unlikely to front run the May 23rd deadline (similar to BTC ETF deadline)

Based on the key dates from the BTC ETF process, we are unlikely to get material updates from the SEC until at least late March. This is at least a month from now and the market is unlikely to interpret any delays as bad news given the expectation of reduced turnaround times compared to the BTC ETF.

SEC issued comment letters on 9/29 (~90 days before deadline)

Equivalent ~2/23

Meeting with issuers ~11/20 (~50 days before)

Equivalent ~4/3

Turning comments on applications and filings early December (~30 days before)

Equivalent ~4/23

The magnitude of inflows into the Bitcoin ETFs reinforces the significance of a potential ETH ETF with some even arguing that more flows into BTC increase the likelihood of an ETH ETF approval in May. I don’t completely agree but at a minimum it marginally increases the expected inflows that would come as a result of an ETF. You have to imagine there is some amount of the BTC ETF assets that would rotate to an ETH ETF. The number might not be 50% but it’s likely not 0%. This should increase speculation going into the event via higher repricing of the asset. As anyone who operates in digital assets knows, once someone touches Bitcoin, their odds of touching Ethereum multiply and ETH is a smaller, less liquid asset that requires less inflows to achieve the same price moves.

Going with the results of my Twitter poll, my base case is that an ETH ETF is not approved, yet this trade still works well. If it were to be approved, I would expect ETH/BTC trades above 0.09 rather quickly (yet another reason why the pair will reprice higher in the meantime).

Bonus Content :)

At the end of my last blog post I included a few charts that I found particularly interesting or gave me some ‘ah ha’ moment. So for those who made it through this whole piece I’ll leave you with some extra alpha.

“But how can you say ETH will outperform BTC even if an ETF doesn’t get approved? BTC will have a continuous advantage via traditional investor inflows.”

Firstly, it is not talked about enough how important Grayscale’s trusts, particularly GBTC and ETHE, were in the last bull market for inflows to the asset class. For reference, GBTC received $6.6B of inflows in the five quarters from Q1 2020 through Q1 2021 while ETHE received $1.2B. Despite GBTC’s flows trumping ETHE’s by 5.4x, ETH outperformed BTC by ~2x over that time period.

I actually find it quite plausible that ETHE trades at a premium to NAV once again prior to its ETF approval. The consensus believes if the ETF isn’t approved in 2024 that it will happen in 2025. Under that assumption, ETHE is cheaper ETH exposure by an order of magnitude compared to the ETH futures ETFs like EFUT. ETHE trades around a ~10% discount to NAV (less 2.5% of annual fees) while ETH futures trade at a 15-20% premium to spot.

The other thing the above table does is show how impactful the ETFs inflows are and will be. Roughly 1.5 months into their launch we are already at ~$5.5B of net inflows.

Some more charts below on the GBTC and ETHE historical share creations below.

Amazing work sir, as always!

Hi Quinn, is there a website and contact details for your fund? Cheers in advance.