Trade Idea: Long GBTC / Short MSTR

Tactical trade idea capturing the closing of the GBTC discount and MSTR premium

Thesis:

The timeline of the Bitcoin ETF being brought forward from an expected 1-2+ years to 1-6 months away, combined with its importance is not yet appropriately understood and priced in by the market. The cleanest way to play an ETF approval is longing GBTC to capture the upside Bitcoin price movement, plus the closing of the discount. Although less of a pure play, COIN is also a method that needs to be evaluated given its role in the ETF and other upcoming catalysts.

Despite the backdrop of positive catalysts favoring Bitcoin and digital assets, the space does not trade in a vacuum. The negative effects of a macro driven and/or broader tech sell-off would present near-term headwinds for Bitcoin and should be considered. Broader liquidity support and favorable investor positioning that have propelled YTD risk asset performance have waned as the Fed appears to be willing to maintain QT and interest rate hikes until something else in the system breaks. Under the belief that Bitcoin would outperform the Nasdaq relative to previous downturns, the best way to hedge this risk is via a public equity.

MSTR is overextended relative to the price of Bitcoin. MSTR’s fluctuation in performance relative to Bitcoin is due to it being one of the few pure play ways for traditional investors to gain exposure to Bitcoin. However, once the Bitcoin ETF is in market it will trade more in line with its fair value as investors prefer a lower cost/higher efficiency alternative, thus losing most of the premium it trades with today.

1. The timeline of the Bitcoin ETF being brought forward from an expected 1-2+ years to 1-6 months away, combined with its importance is not yet appropriately understood and priced in by the market.

A key component being overlooked by the market is the magnitude in which the ETF unlocks of access for traditional institutions who manage the vast majority of the world's assets. Despite self-custody being a huge FEATURE for digital assets broadly, it is a BUG for institutions in today's environment. We are a long ways away from it being translated into workable infrastructure that satisfies the legal, compliance and regulatory needs of asset managers.

This recent study from PwC highlights this exact issue. The ETF unlocks this overnight starting with BTC and eventually other digital assets. From there, institutions will continue to educate themselves and better understand the benefits of self-custody. Improved infrastructure solutions will then be demanded and built over time so they can eventually self-custody themselves.

It is also interesting to look at the historical comparison to when the first gold ETF launched in 2004. I discuss that and why GBTC is a great way to play the outcome in a deeper dive here. Despite the GBTC discount being at its lowest level in almost a year, it still sits at a 28% discount to NAV, implying a 39% return if held until par.

For completeness, COIN also stands to greatly benefit from a positive ETF outcome as it is an integral component to all of the ETF applications with both the surveillance service agreements and custody business to hold the underlying Bitcoin. Coinbase is the most diverse business in the digital asset ecosystem with leading product lines spanning layer 2 Ethereum scaling (Base), institutional and liquid staking (cbETH), stablecoins (USDC), spot and derivative trading volumes (exchange) and asset custody. Reading between the lines of the SEC’s newly softened stance towards the Bitcoin ETF, Coinbase will stand to benefit from any additional regulatory easing, constructive legislation, crypto-friendly political candidates and a potential Ripple victory versus the SEC. I called for its breakout relative to Bitcoin here.

2. Despite the backdrop of positive catalysts favoring Bitcoin and digital assets, the space does not trade in a vacuum. The negative effects of a macro driven and/or broader tech sell-off would present near-term headwinds for Bitcoin and should be considered.

In addition to the Bitcoin ETF, I see other drivers providing support to digital assets over the coming 12 months that include:

More supportive political and regulatory environment as governments are forced to compete globally for entrepreneurs, talent and innovation. In the US specifically, ahead of 2024 elections the tide is shifting among presidential and congressional candidates who are becoming more constructive towards the space.

Stablecoins have proven to be one of the most important use cases for digital assets as they are a global improvement to the existing standards across currencies, payments and money transfers. Supply across the two major stablecoins, USDC and USDT, has been flat for 8 months and appears to be forming a bottom. The technological upgrade from the fiat banking system to digital dollars is recognized by all who use them for the first time, including central banks where 86% of them are actively researching CBDCs.

Ethereum’s proof of stake upgrade provides the most tangible valuation framework across the digital asset ecosystem that can be understood by traditional investors. This provides a critical launchpad into better understanding the many applications built on top of Ethereum and other networks that can also be valued, understood and compared to traditional business models.

Broader digital asset adoption will continue in ways we can’t yet predict or visibly understand. With more than half of the Fortune 100 developing blockchain initiatives as detailed by a recent Coinbase study, user growth and the embrace of this new technology is a one way street. It’s important to note how quickly innovations can be adopted and spur new growth. An example I’d point to is from this May 2022 CoinMetrics Report which shows that in less than a year transaction volume of the newly released ERC-721 token standard (NFTs) went from basically zero to surpass the volume of existing ERC-20 tokens.

On the macro front, my near-term precautions are outlined in this recent piece. In short, I believe the easy part of the Fed’s fight against inflation is over and the constraints of their ‘rock and hard place’ reality will reemerge. In short, the decoupling of the Nasdaq and long duration treasuries is not sustainable in my mind.

I also find the rising initial jobless claims to be a red flag and something to be monitored.

For reasons such as this one, I don’t believe the Fed has much of a choice when push comes to shove in saving the economy/markets or fighting inflation/currency debasement. Basic incentives will always motivate decision makers to kick the can and cave in to stimulus so their legacy is not the one which caused a severe recession. Those decisions still don’t come lightly though and require market crashes and volatility to hide behind (ie March 2023).

I find this 6 year log chart of Bitcoin relative to the Nasdaq extremely interesting and have a positive medium- to long-term view on the direction it goes.

One more point I’d like to call out that gives me pause on the ability of a sustained digital asset rally without a more favorable macro backdrop is the ratio of stablecoin market capitalization to the market capitalization of the rest of digital assets. I highlight this in greater detail here, but the ratio carries a negative correlation to prices - meaning that when the value of stablecoins is low relative to the total digital asset market value, there is a lack of capital inflows which is a headwind for digital asset prices broadly.

3. MSTR is overextended relative to the price of Bitcoin.

MSTR is currently sitting ~25% above its 100 and 200 DMAs relative to Bitcoin.

Here is a quick back of the envelope MSTR valuation model (kudos to whoever made it as it wasn’t me). The true premium relative to intrinsic value at which MSTR trades depends on a number of variables but can be estimated. The moral of the story is the underlying business has become a smaller component over time as its performance has been flat and Bitcoin holdings have increased. The two largest drivers of the premium in share price over intrinsic value is the lack of Bitcoin investment vehicles for traditional investors and the embedded call option on the price of Bitcoin provided by the company’s use of leverage. In addition to the downward pressure from the ETF, the premium will also fade over time as the company’s leverage decreases via additional share issuance to acquire more Bitcoin and the convertibility of ~77% of notional debt as prices increase.

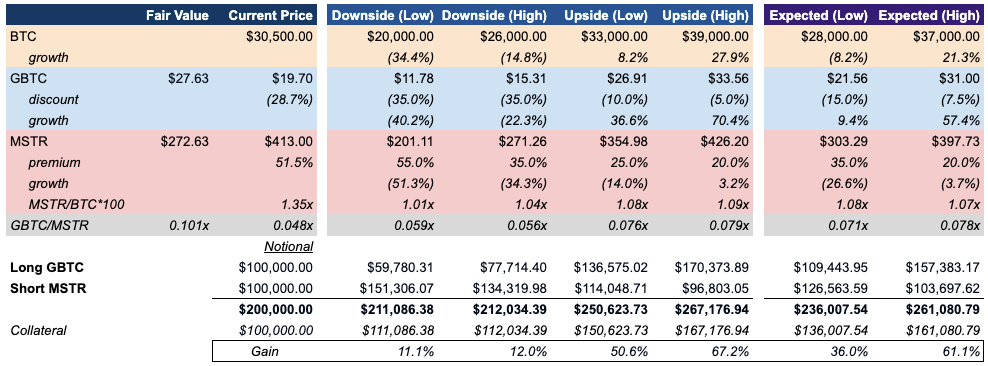

When coupled with the MSTR’s inherent beta to Nasdaq, if structured appropriately MSTR presents a useful vehicle to hedge under these expected conditions. The setup is such that as the Bitcoin ETF becomes more likely, the embedded premium in MSTR shares will decrease while the GBTC discount closes. There is ~30% upside on both sides of this trade to be captured which could equate to a +60% gain if you’re able to execute without having to post excess collateral (also excludes funding costs and fees).

Trade Structure:

There’s a number of ways you could execute this thesis depending on your preferred exposure. The table below highlights my preferred method which is a 1:1 equal notional long GBTC / short MSTR. If all goes as planned, you stand to outperform the price of both Bitcoin and GBTC in both upside and downside scenarios.

My base case for BTC on an ETF approval is a rally to the top end of this $33,000-$39,000 range, with a potential downside around the 200 DMA at ~$26,000.

Your downside feels like a GBTC/MSTR ratio of ~.04 based on historical lows, and that would require a significant re-widening in the GBTC discount and presumably that would also be bad news for MSTR and the price of Bitcoin broadly which would serve as your hedge.

Historically the GBTC/MSTR ratio has been pretty negative to uncorrelated with the price of BTC.

There appears to be ample MSTR short borrow with regular margin costs, but if that were to become too expensive, an additional method could be to sell ‘covered’ MSTR calls against your GBTC position. You are less hedged in a downside price movement here but stand to benefit if volatility remains low. Which strikes you decide to sell will determine the payout structure. Option expiry is also an important factor here to consider which could play out in your favor or against you. The short equity approach feels safer from a duration perspective if MSTR were to keep running. The benefit of the selling calls approach would be the additional yield gained if prices remained relatively unchanged while you collect the option premium.

I welcome any and all feedback! Please don’t hesitate to reach out via email or on Twitter.